Sunday Letter

A Tale of Two Economies

Dear reader, Markets have been on a tear this year. The US S&P 500 is up 26%. Many economic indices look like they are doing just fine. Ray Dalio and Bridgewater, however, argue that the US economy should instead be split into 2: the Top 40% and the Bottom 60%. While statistics averaged across the whole US economy can be deceiving, when the economy is split into those two segments, the numbers tell a very different story.

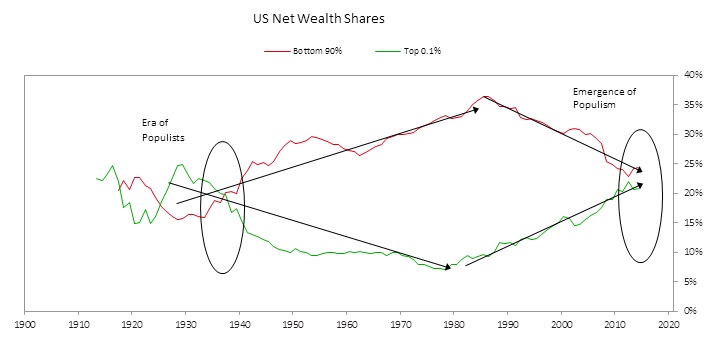

The chart below shows that the wealth of the top 10% of the population is equal to that of the bottom 90% of the population: same as during the 1935-1940 period.

The Top 40% now has 10x more wealth than the Bottom 60%. In 1980 it was 6x.

Two-thirds of the Top 40% save part of their income; two-thirds of the Bottom 60% save none.

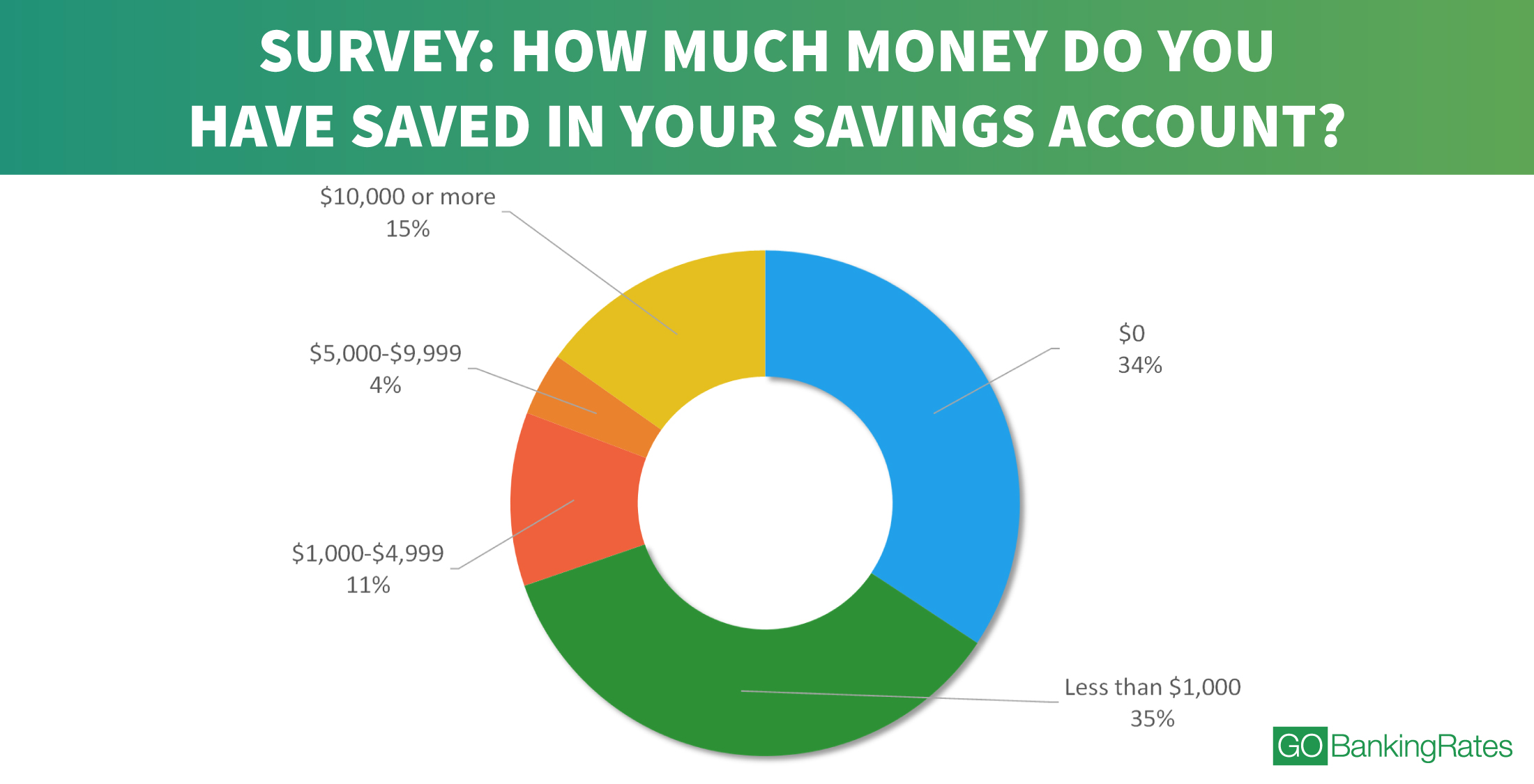

The chart below shows that 69% of people in the US have less than USD 1000 in their savings account; 80% have less than USD 5000. Note that this is not the amount that they have saved for emergencies: this is their total cash savings. A recent Federal Reserve study shows that the Bottom 60% of people would struggle to raise even USD 400 in an emergency.

The Top 40% even live longer. Premature deaths among those in the Bottom 60% are up 20% since 2000. They are twice as likely to die of premature death. In contrast, life expectancies of the Top 40% are longer than ever.

Why has this schism in the US economy happened? While there are many reasons, one large factor is simply that the US economy is trending towards higher-skilled (and higher-paying) jobs, but fewer of them. As Mark Zuckerberg famously said, a skilled engineer is worth 100x an average engineer. Continuing trends towards automation and digitisation are further intensifying the effects on employment and the wealth gap.

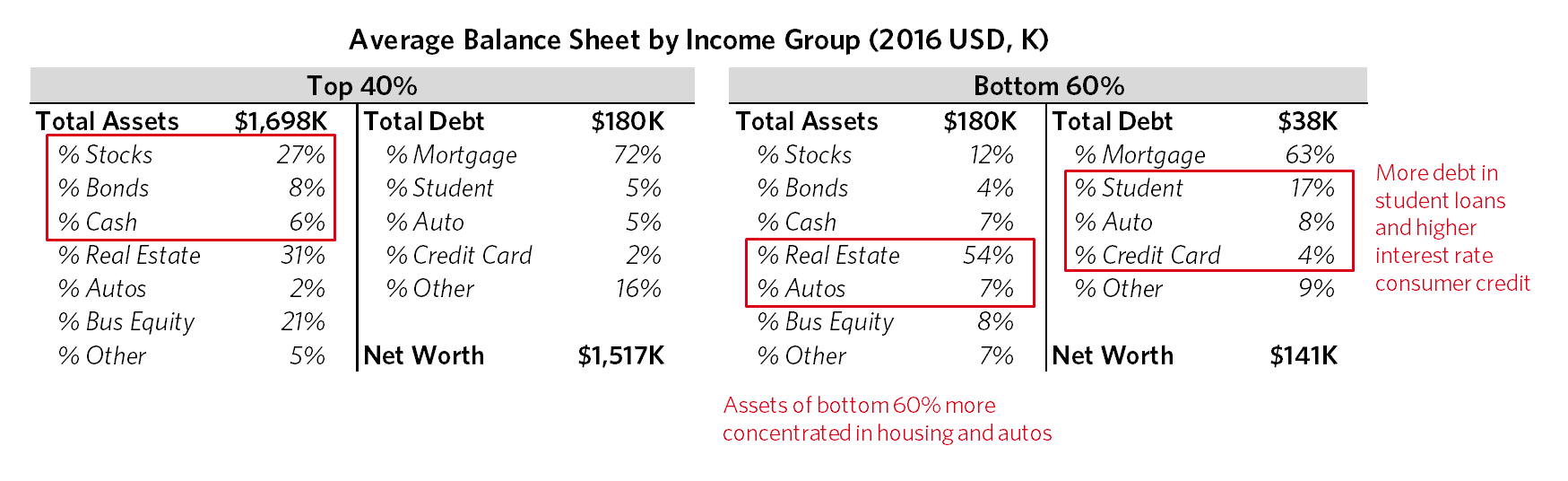

The Top 40% have also benefitted from changes in asset values (being the asset owners). The Bottom 60%, owning no assets, have only their incomes to rely on: and real household incomes for them since 1980 have been flat. Likewise debt of the Bottom 60% is skewed towards more expensive forms, such as student loans and credit card debt.

Should the Fed and the US government be trying to run two separate sets of policies, to take into account these two different economic segments?

One thing is for sure: the burgeoning divide between these two economies will define both US politics and economics over the next decade. The reverberations from this showdown will be felt across the world.

Yours Sincerely,

Henry Chong