Sunday Letter

Earthquakes

“If a financial crisis comes every 5 to 7 years, why are people always so surprised when it happens?”

– Jamie Dimon’s Daughter

Dear reader, No one likes losing money. A principle of decision theory is loss aversion: people will do more to avoid a loss, than they will to obtain an equivalent gain. This is closely linked to risk aversion, and is why insurance companies can make money. Risk-averse individuals will pay risk-neutral insurance companies to bear the risk instead.

And yet, when I was recently in Hawaii, I saw many houses built right on top of old lava flows, from active volcanoes. Likewise people rebuild their homes in the flood zones of Florida in exactly the same spot after each hurricane.

It is difficult, if not impossible, to predict exactly when another volcano eruption or hurricane will hit. But hit they will: sooner or later.

West Texas Intermediate (WTI) Crude Oil lost 75% from Peak in June 2014, to Trough in February 2016

Supply and demand in most markets is usually fairly balanced, at a given market clearing price. It only takes tiny demand/supply imbalances to persist in order to drive these dramatic price swings. In 2014, a 2% differential between demand and supply for oil led to a collapse in oil prices. Predicting in advance when such swings will happen is hard. Predicting that sooner or later such swings will happen is easy.

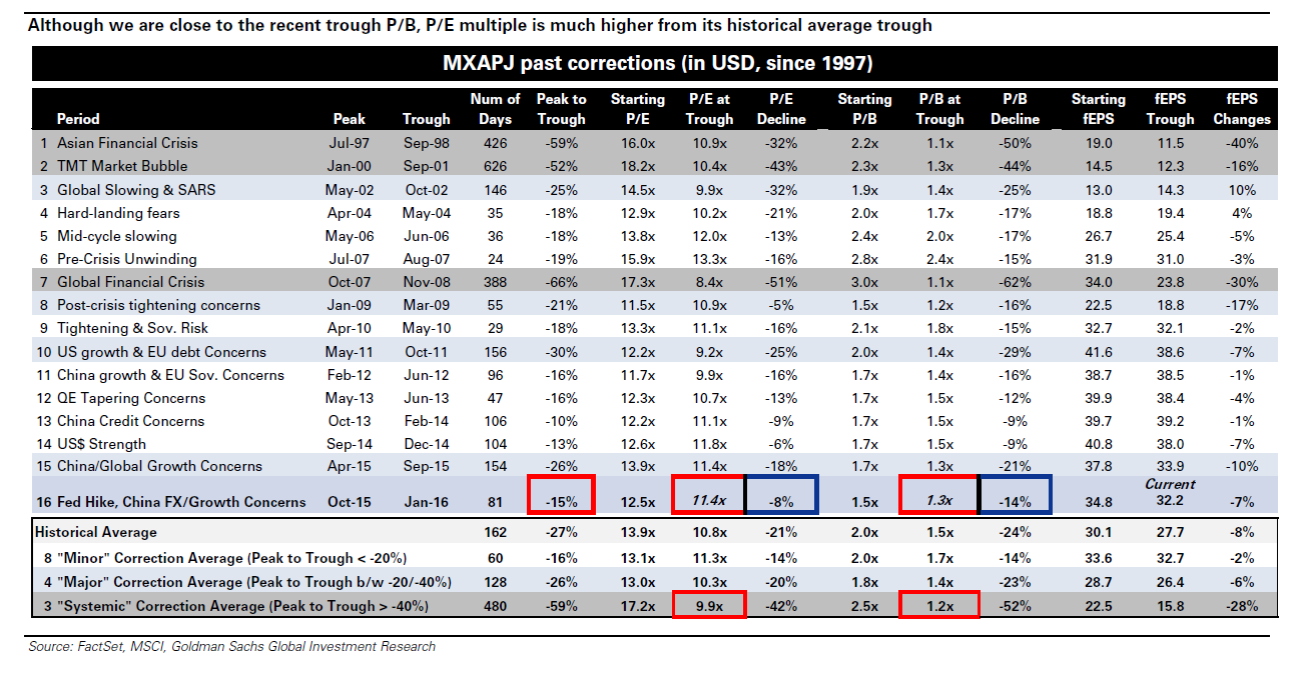

People often only remember big market crashes, when every newspaper and TV commentator is weighing in. But markets experience swings more frequently than people might realise. The below chart shows instances over the last 20 years where the MSCI Asia Ex-Japan Equity Index has fallen more than 10%.

Double-digit declines in the Asian equity markets happen more frequently than people realize

If you were to invest at the trough of each of these points, you would have done very well for yourself. The problem is that tables are easy to construct in hindsight. It is tempting to say that investing is easy: just buy low, sell high. The problem is figuring out whether a market is indeed low or high. Especially because everyone else will be doing the opposite of what you believe.

It’s easy to tell when an earthquake has hit; it’s harder to tell when markets are at a high or low.

Furthermore, people’s asset allocations do not take into account what happens when a major “earthquake” hits. Asset classes tend to become correlated during corrections. In 2008, correlations among major asset classes and the S&P 500 tended towards 1 (Dalbar 2016).

So how do we go about having an asset allocation that can help weather those storms, and husband the courage to invest when circumstances are favourable?

Yours Sincerely,

Henry Chong