Sunday Letter

Investment Fallacies: Bonds & Ladders

Dear reader, Another piece in my series on Investment Fallacies.

Many investors believe that “you should own bonds directly, not bond funds, because bond funds can fall in value but you can always hold a bond to maturity and get your money back.”

Bond funds are, ultimately, a collection of individual bonds. They are just portfolios that are marked to market every day. They are, therefore, also a collection of the idiosyncratic risks of each of the underlying bonds. At any given day, you can swap a bond fund for a portfolio of the underlying bonds, and vice-versa: regardless of movements in price or rates.

It is indeed true that individual bonds mature, and that investors “get their money back” (assuming that there is no default risk) if they just hold on to the bond long enough. In reality, however, getting nominal dollars back when a bond matures shouldn’t excite anyone: what matters is whether or not your purchasing power has been maintained.

Let’s say interest rates go up. It is indeed true that the value of the bond fund will fall. But so will the real purchasing power of the nominal dollars you get back when your bond matures.

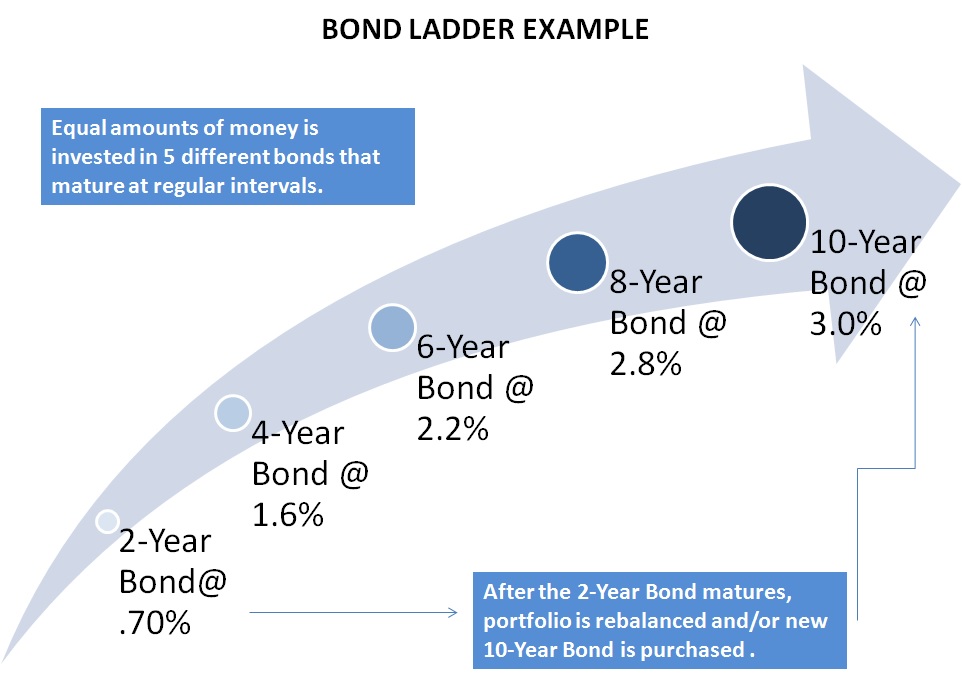

Furthermore, as each bond matures, unless investors choose to hold the resultant cash (an asset allocation decision), they usually will reinvest it at the far end of the “ladder”. Thus while each individual bond may indeed mature, the portfolio as a whole never does.

In the example above, instead of purchasing a spread of individual bonds at various maturity dates, you could instead buy a bond fund investing into only 10-year bonds, and redeem periodically from that fund in order to generate income/cashflow.

To be fair, investing at the far end of the yield curve exposes you to greater interest rate risk, but that is a separate discussion.

Note that I am not necessarily advocating purchasing any particular bond funds. Indeed, many actively managed bond funds don’t do particularly well. Simply that the choice of instrument of individual bond, or pooled fund alone, should not be a factor.

Furthermore, investors need to realise that when they purchase a bond they are in fact making a number of simultaneous “bets”, including credit risk, interest rates, currency, and the movements of the bond market as a whole. All of those factors can and should be separated out. If you don’t have a particular view on, for example, interest rate movements, then that factor should be hedged out: if not at the individual bond level, then at the portfolio level.

Yours Sincerely,

Henry Chong