Sunday Letter

The Digital Asset Revolution

Dear reader, Blockchain technology has taken the world by storm. Discussions of cryptocurrencies play constantly on Bloomberg and CNBC. But is it all hype? What are the real-world applications of blockchain technology?

So far the main use-cases of blockchain have been fund raising (Ethereum) and the transaction of value (Bitcoin).

I personally believe that in many ways the blockchain industry right now parallels the internet industry in 1997. 95% of companies in this space have broken business models at best, and are frauds at worst. Nevertheless, the underlying technology is truly revolutionary.

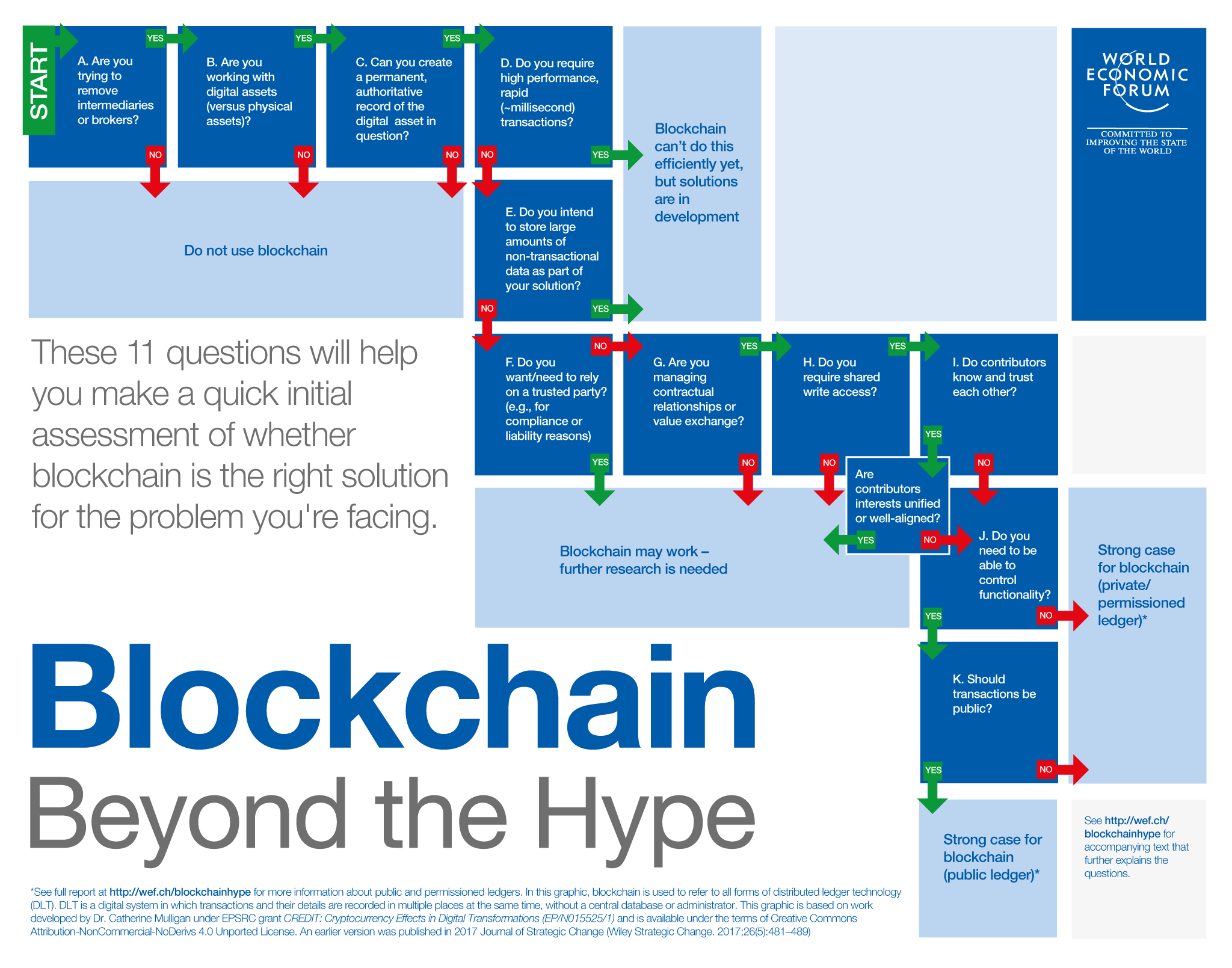

Below is a flowchart from the World Economic Forum detailing when a blockchain does and does not make sense. As I’ve written about before, blockchains only make sense when you need decentralisation, immutability, and trustless verification. Otherwise, a traditional relational database makes more sense. For example, if Gucci wants to allow users to verify whether or not a handbag is authentic, they can include a QR code inside the handbag that queries a central database. As Gucci is the sole and final arbiter of what is “authentic”, there is no need for either decentralisation or trustless verification.

Ideas are cheap; execution is everything. Companies that can actually build real-world use cases have the potential to be the next $100 billion companies that will dominate their industries.

One fundamental challenge facing the cryptocurrency industry is the difficulty of converting fiat currencies into cryptocurrencies, and vice-versa. The two worlds exist almost entirely separately. For this industry to succeed, bridges will need to be built to allow the two worlds to interact, if not merge in future. All the same legal and regulatory requirements that fall upon people who transact in fiat currencies should be applied to those transacting in cryptocurrencies, including Know-Your-Customer (KYC) and Anti-Money Laundering (AML) rules.

Today, just a small handful of banks such as Silvergate and Noble handle almost all of the fiat transactions related to the crypto world. They have grown explosively in the last 12 months. This represents a massive vulnerability in the system. As those banks do not have their own direct correspondent banking relationships, if any of the US-dollar clearing banks decide not to work with them, funds at most exchanges and intermediaries will become frozen.

Institutional “on-ramps” have to be built to bridge this gap, allowing investors access to the market in a regulated fashion, through a familiar vehicle, such as an index fund.

Not that long ago, stock exchanges had separate “paper” and “electronic” trading sessions. Today, it’s just all trading. Similarly I believe that in the near future we will stop referring to “digital assets”: all assets will be digitally represented in token form. Next week, I’ll look in more detail as to the classification of different kinds of tokens, and why I believe that Security Tokens will soon be a term on everyones’ lips.

Yours Sincerely,

Henry Chong