Sunday Letter

The Unicorn Hedge

“My dear, here we must run as fast as we can, just to stay in place. And if you wish to go anywhere you must run twice as fast as that.”

– Lewis Carroll, Alice in Wonderland.

Dear reader, The quote above, from Alice in Wonderland, is often used to refer to what evolutionary biologists call the Red Queen Hypothesis. In short: all organisms must constantly adapt, evolve, and proliferate: not just to gain an edge on other species, but just to keep pace in an ever-changing environment.

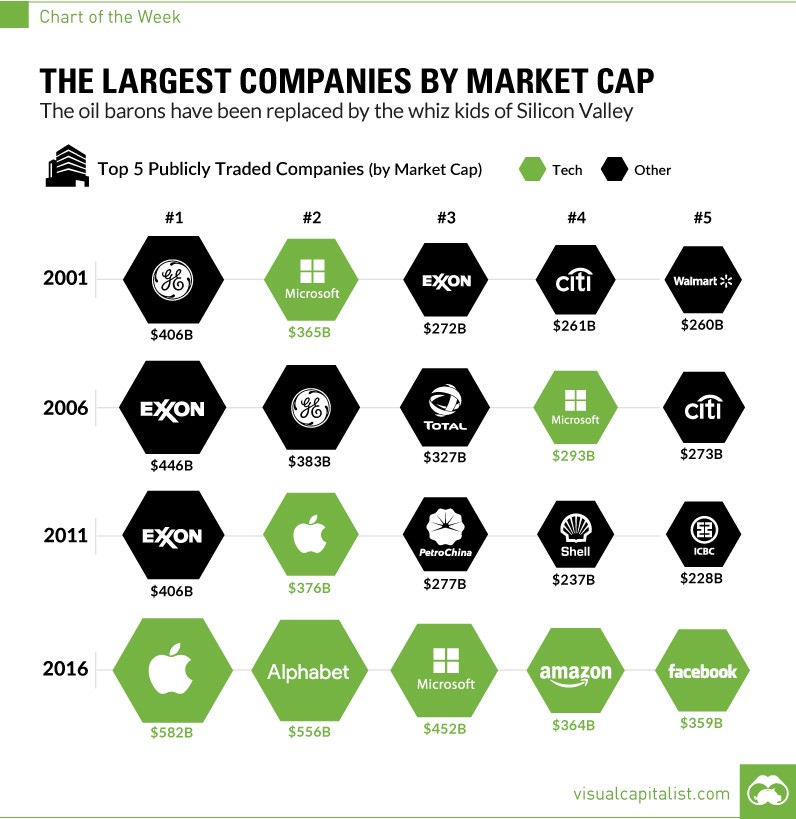

In 2011, Marc Andressen wrote an article on how “Software Is Eating The World”. Back then, apart from Apple, the largest companies in the world by market cap were the oil majors and banking giants. Today, as he predicted, the largest companies in the world are all technology and software companies. Even companies such as Amazon, which makes the bulk of its revenue by selling physical goods, are fundamentally driven by the combination of software and data.

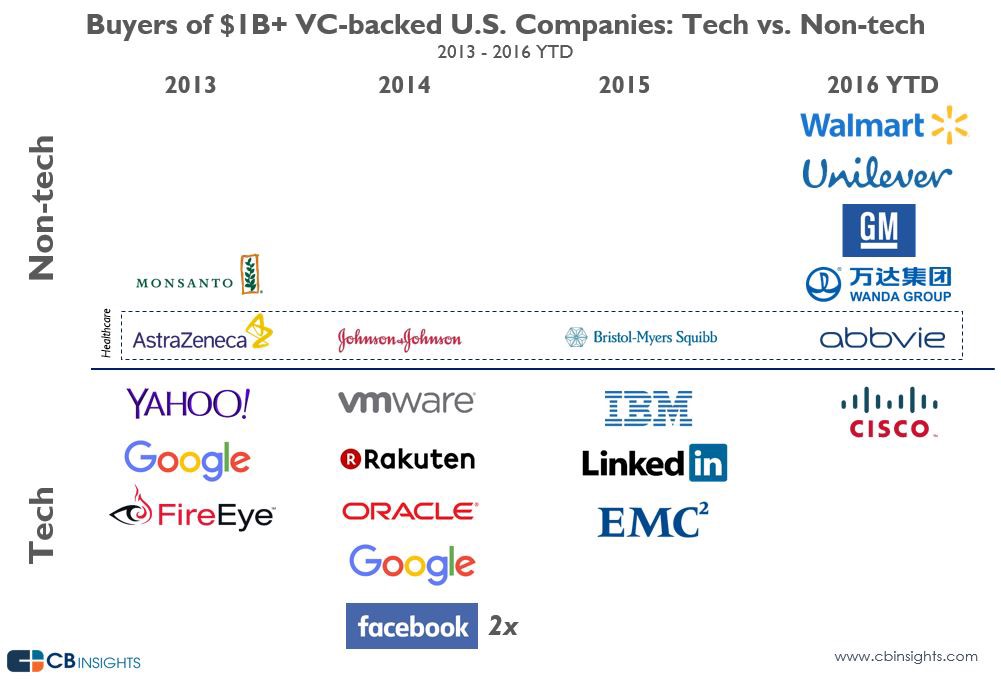

Dave McClure of 500 Startups wrote about “The Unicorn Hedge”. He argues that more and more business models are being rapidly disrupted, and that the real “bubble” is not in new tech startups, but in the currently high PE multiples of large global public companies operating in “traditional” industries.

As more and more such companies realise the impending threat from these new insurgents, McClure believes that many of these public companies will attempt to hedge their valuations by buying-out these disruptive companies.

For example, he argues that if large automotive companies today don’t rapidly innovate, they won’t just be overvalued, but will cease to exist, as electric and autonomous vehicles become the norm.

Facebook has been one of the most aggressive companies in identifying potential threats to its business, and either buying them out, as with Instagram and WhatsApp, or rapidly copying features itself, as with Snapchat. In doing so they have grown to become the social media giant they are today (for better or for worse). The combination of being a strong, visionary founder with the fact that he owns a majority of voting rights in his company has allowed Zuckerberg to move as aggressively and rapidly as he has. Likewise with Jeff Bezos and Amazon. The mere potential of Amazon entering a market sends the stock prices of incumbents crashing, as it has recently with the Pharmaceutical industry.

On the other hand, many banks today do not have a single controlling owner. Bank CEOs must navigate both internal politics and external regulation: with the result being a dramatic lack of innovation.

Zuckerberg today is 33 years old. The scary thought is that he could be at the helm of Facebook for many years to come. How can incumbent “traditional” businesses expect to compete with that without dramatic and rapid innovation?

Yours Sincerely,

Henry Chong