Sunday Letter

Token Classification Framework

Dear reader, In the past few weeks I’ve written about the challenges facing the blockchain industry, the market potential during a gold rush, and the current digital asset revolution.

This week, I will explore the different kinds of digital tokens out there. Such distinction, both technological and legal, is essential to an understanding of the digital asset market and its future.

At the most reductionist level, a token is either valued intrinsically, or as a representation of something else, such as an asset or in exchange for a service. Technologically, all digital tokens now are bearer instruments: whoever “holds” them and has possession owns them. This is in stark contrast to most financial instruments today, which are registered instruments: they may be legally or beneficially owned by you, but are rarely actually in your possession. An example of this are most equities. When you buy Apple stock, you don’t actually hold a stock certificate: a custodian does that on your behalf.

This has far-ranging ramifications. Beyond the security aspect (you’d better make sure you keep possession of digital tokens safe at all times), the truth is that the financial world is no longer set up to deal with bearer instruments. Just try walking up to your local bank branch to deposit a bag of cash, or a stack of bearer bonds, and see what happens. In fact, beyond the cash in your wallet, land titles in certain countries, and perhaps some gold bars in your home safe, almost nothing you own is in bearer form anymore.

You may think that the money you have in your bank account is “yours”, but in truth it is being held on your behalf by the bank. It is “registered” in your name. Withdrawing that money requires the bank’s approval. I will discuss how to deal with bearer digital tokens more in next week’s letter.

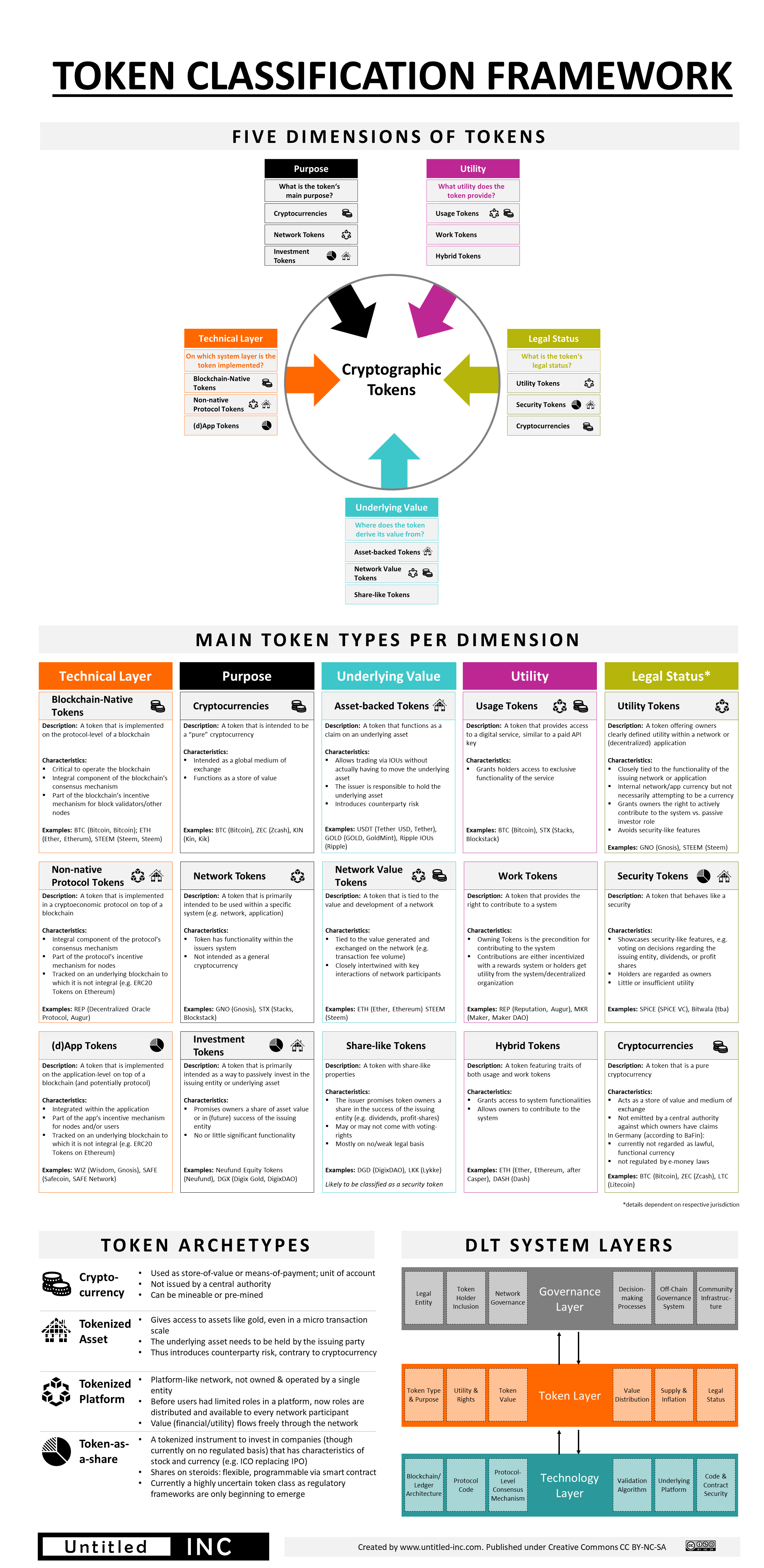

Below is an infographic outlining different dimensions of tokens, and some examples of each (click on the image to enlarge):

At Fusang we have come up with a 5-part legal classification for digital tokens.

1. Virtual Currencies/e-Money

Virtual Currency, or Electronic Money (e-Money), is simply a digital representation of fiat currency. For example, Starbucks Dollars stored in their app, or Hong Kong Dollars stored on the Octopus cards used on public transport. e-Money is treated by most regulators in the same way as regular fiat money, additionally requiring an “electronic wallet” or “stored value” licence, and is subject to the same rules and regulations.

2. Cryptocurrencies

Cryptocurrencies are tokens that function primarily (and arguably solely) as money. Specifically, they have to meet the classical economics definition of money: (1) a Medium of Exchange, (2) a Unit of Account, (3) a Store of Value. Tokens such as Bitcoin and Litecoin meet that definition, as might others in time. Given that it remains extremely difficult and rare to exchange cryptocurrencies for real-world goods and services, true cryptocurrencies remain few and far between.

If a token is indeed defined as a cryptocurrency, while it may not be subject to taxation (depending on the jurisdiction), it is important to remember that currency transactions are still heavily regulated. All intermediaries have a duty to ensure that the money they touch is not the result of ill-gotten gains or money laundering.

3. Utility Tokens (ICOs)

Utility Tokens, popularly known as Initial Coin Offerings (ICOs), allow holders to exchange them for services or access. For example, Filecoin allows users to access a distributed file storage system. FINMA (the Swiss regulator) has stated that a Utility Token must have utility at the point of issuance, for it to be defined as such.

Unfortunately, most ICOs today are used primarily as fund-raising mechanisms. While I am sure that pure utility tokens exist, apart from Bitcoin I have yet to see one. Nevertheless, there are a number of companies working on projects that can have clear utility. For example, Amazon is exploring issuing their own digital currency. Amazon’s net profit margins are 2-3%; the merchant fees they pay whenever a customer uses a credit card to make a purchase are 2-3%. By internalising the whole transaction process, Amazon can double their net profit margins. Amazon will not need to raise any money from an initial sale of the token: it will truly have pure utility.

It is important to realise that even if an ICO is not a security, and is treated essentially as a “pre-sale” of goods or services, it will probably be subject to corporate income tax (like any company income). Especially if a company is based in a high-tax jurisdiction, this means that a large chunk of ICO proceeds could be swallowed up on day one: a fact that I imagine would give many investors pause.

4. Security Tokens (ISOs)

I believe that Security Tokens, or Initial Security Offerings (ISOs), will come to dominate the digital token space. These are tokens that represent securities such as equities, debentures (bonds), or collective investment schemes (funds).

I do not believe that these should be treated or regulated any different than their underlying securities. The fact that they are now represented by a digital token simply helps with the trade, clearing, and settlement process – much as with the shift from paper securities to electronic securities.

The US has the Howey Test for what constitutes an investment contract, while countries such as Singapore and Hong Kong have similar tests for collective investment schemes. Broadly, there are four relevant elements: (1) an investment of money, (2) collective pooling of assets, (3) that the investor has no direct control over, and (4) an expectation of profit or financial gain from that investment.

That last test in particular is pertinent: most people “invest” into ICOs, presumably with expectation of financial gain. I am not sure many people would put money into an ICO that explicitly advertises the impossibility of financial gain. In contrast, no one tops up their Starbucks cards with hopes of one day striking it rich.

5. Asset-Backed Tokens (ABTs)

ABTs represent real-world assets, such as gold bars, art, commodities, and real estate. ABTs in theory allow for fractionalised ownership: you could now own some small fraction of a Monet. Even more interesting than ISOs for asset classes such as equities are those for real estate: by far the largest asset class in the world.

In practice, we believe that ABTs will be rare: even if a token represents a real asset such as real estate, most countries will define them as collective investment schemes, making them Security Tokens, as there is an operator managing the real estate on your behalf (thus meeting all the tests for being a security listed above).

It is important to remember that it is not up to the token issuer or purchaser to define the legal status of a token: the courts will do that, with an examination of the facts, following guidance from regulators. It’s further important to realise that securities violations are treated with extreme severity by most jurisdictions. In the movies, that’s when men in windbreakers kick down doors at night. Many token issuers are hoping that if regulators deem their activities illegal, they will repent and reform. Unfortunately, in many cases it will be too little too late.

Regulators have FOMO like the rest of us, and many are adopting a “wait-and-see” approach. When (not if) the tide of clampdowns come, however, it will lead to a healthy washing-out of the industry. What remains will be the companies who have been fully compliant and have focused on building real-world value for their customers.

Yours Sincerely,

Henry Chong